On data centers

Wherein the author "wet blankets" with abandon

The current data center buildout is probably a waste of money. We’re going to look back on this period and shake our collective heads or rub our chins with wonder: never has so much money gone to so little purpose so quickly. (Not since the money hole, that is.) That we’re in the midst of an “AI” bubble is patent—even the participants in the bubble can see it. Many even recognize echoes of the dot-com crash around 2000, which is slightly less obvious since a lot of the tech community were children or not-yet-born back then and the facts of that collapse are more obscure. But everyone seems to think that this time is different because “AI” is transformative and The Future so maybe this bubble is more B’loonies—think Super Elastic Bubble Plastic if you’re older—than soap. (We’ll save “AI” as such for another essay since we have to show its soapiness here.)

The scale of the capital expenditures is sui generis. There is nothing like it historically (in peacetime): the transcontinental railroad cost about $1 billion inflation-adjusted and the dot-com-era fiber buildout was probably about $500 billion. We’re obviously still in the midst but it’s estimated that the big players have spent over $1 trillion so far with $4–8 trillion from here. (WWII mobilization is estimated at $5 trillion.) Unlike past frenzies, this one’s largely equity-financed rather than debt-based. That speculation—equity’s junior to debt in obligations—has supplanted usual investment patterns and increased the cost of capital economy-wide (if it’s even available).

The specifics of this bubble are not philosophic in nature so they’re beyond the purview of this essay, but they have been ably covered elsewhere. Each of these analyzes the business side of “AI” with well-sourced, objective essays. (They’re variably rant-y but it’s “hard to keep your head while all about you are losing theirs” all the time.)

Ed Zitron’s “Where’s Your Ed At?” in general but specifically:

One aspect of the bubble analysis that I haven’t seen discussed is why. Perhaps it’s because we’re in the midst of it and most causal analysis happens afterwards, but no one seems particularly interested in determining how we got to here.

The cause is President Joe Biden’s COVID-era monetary inflation. No doubt in my mind. It has just taken a while to play out and it came out in two spurts.

If you remember during COVID-19, the federal government—starting under Trump but accelerated by Biden—dispensed egregious amounts of taxpayer money while the Federal Reserve expanded its balance sheet prodigiously.

Ludwig von Mises’s theory of inflation-induced booms is that they hit producers first. In his reckoning:

The foregoing statements explain why an expansion in the production facilities and the production of the heavy industries, and in the production of durable producers’ goods, is the most conspicuous mark of the boom.1

The basic idea is that the government expands the money supply, which predominantly takes place as an extension of credit to the banks. These banks then use that money to invest or lend, primarily to the production side of the economy. This cheap, ready availability of credit is nominally a signal to producers that their neck of the economy is growing and it’s worthwhile to expand production to meet the expected demand increases.

When the demand doesn’t materialize (or doesn’t in time) then the producers go bankrupt, start merging, lay workers off, shed assets, and try to survive. This is the bust part of the cycle and there have been many in my lifetime. Until the bitter end, there are people saying “this is fine.” Afterwards, others start pointing: either to their Cassandra-like calls or their fingers at not-them that are responsible for the “events that are unfolding currently.” The average person just face-melts.2

To my mind, this unfolded the way it has because this usual bust-y path was delayed by COVID-era direct cash payments, loan forgiveness, eviction restrictions, and unemployment support. The banks, flush with cash in the form of reserves, sat out the producer-lending part while the consumers went bananas in the part of the economy that is usually a lagging indicator.

Thus the Biden-flation. It was in all the sectors that a growing economy supports—luxury goods, homes, gas, automobiles, groceries, restaurants—but blown up by an air compressor rather than the lungs of organic growth that won’t go too far. Each of those areas suffered stagnation or collapse with rampant layoffs to release the pressure.

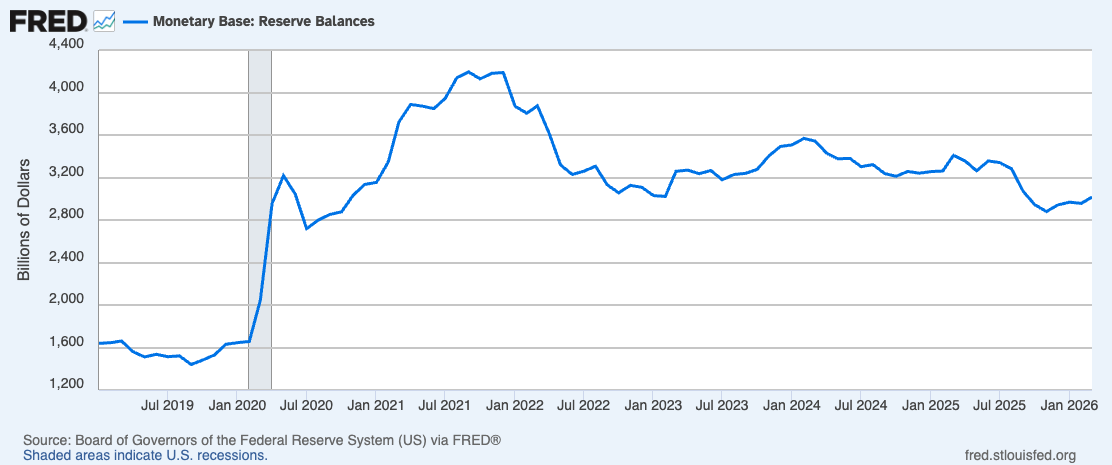

Meanwhile, the banks mostly sat out this period because of its volatility and then thanks to the Federal Reserve’s unprecedented interest on reserve balances. Why lend to these consumer-facing sectors when you can earn a comfortable return doing nothing?

The “AI” bubble started once there became higher-return opportunities for the banks. Reserve balances started dropping but stayed at a level closer to the start of the pandemic thanks to the Fed’s incentive.

So where did the banks’ excess reserves come from and then disappear to? I think you know. This period coincides with the rise of private credit, private equity, and the dizzying valuations of the “tech sector,” especially NVIDIA and its customers.

It also coincides with the rise of the “tech sector” backlash, of which the data center Luddism is the latest fashion after “climate change” became déclassé. Its costume is the usual fearmongering but the wearer is the same collectivist as always.

The three styles that this current fashion takes are the following:

Stealing “our” water and electricity

Attack the data centers at the local level via permit litigation and public meeting activism

Wealth tax

Countering these three is beyond the scope of this essay since doing so takes factual arguments and political activism. There are a couple philosophic things to point out, though:

The data centers’ inputs are not “ours” to dole out or control. It is certainly true that the water and energy systems are currently under governmental—or quasi-governmental—control and apportionment is far more public than it should be. But they have every right to purchase those inputs at “market” rates as those who would restrict them. One captivating idea that’s arisen from this is the idea of “consumer-regulated electricity” and it’s, frankly, the most original reform I’ve come across in the sector:3

Senator Tom Cotton’s DATA Act

Permitting reform and administrative state dismantling are sorely needed and seem to have finally found a smidgen of bipartisan consensus and some Supreme Court success while the activists have had some effects at the local level

The California wealth tax might be a union effort at browbeating Governor Gavin Newsom but that game of chicken might end with it on the November ballot. If enacted, it’s going to be the Bizarro Prop 13 and a thorn in the California right’s (such as it is) side for generations. It’s going to metastasize into something more like a “Success Tax” as the state’s hunger for funds becomes insatiable4

Ultimately, the right to property entails the right to incinerate capital as long as there’s no fraud involved. Though unfortunate, the “AI” bubble with its malinvested data center buildout isn’t up for public vote or governmental veto. The remedy for the other side of the transaction is bankruptcy: if the counterparties financed debt, then they’ll get whatever is salvageable of the stranded assets; if the counterparties took equity in exchange for capital, then they’re going to learn an expensive lesson. (Again, for many of the venture capitalists that have financed past tech bubbles.)

Mises, Ludwig von. Human Action. Auburn, AL: Ludwig von Mises Institute, 1998. 557.

The “foregoing statements” span many pages and rely on a disquisition about the nature of interest that is way beyond the scope of this essay. Here is a taste to link it to monetary expansion.

The main deficiency of all attempts to explain the boom—viz., the general tendency to expand production and of all prices to rise—without reference to changes in the supply of money or fiduciary media, is to be seen in the fact that they disregard this circumstance. A general rise in prices can only occur if there is either a drop in the supply of all commodities or an increase in the supply of money (in the broader sense). (551)

This is perhaps the greatest single comic I’ve ever come across. I have it framed on my wall and each panel is useful in its own right, not just the “this is fine” one.

In a nutshell, the reform is to eliminate energy-related regulation when an electricity-generating source is “islanded”—that is, not interconnected to the grid in which it’s sited. Data centers (and any other heavy electricity users) could own or contract their own generation sources without the headache of oversight.

This permissionless activity could spur economy-wide ramifications, especially if Wickard v. Filburn is overturned (or subverted) by the sure-to-be-appealed Sixth Circuit decision in Ream v. Bessent.

There are two immovable objects at work here: generous, lifelong public pensions and retiree entitlements on the one side and generous welfare benefits and NGO sinecures on the other. The irresistible force is economic and budgetary: people are fleeing California, which would be accelerated by a success tax, and there will come a time of shortfall.

Given these two “objects’” penchant to vote and penchant for riot, their inexorable meeting is going to be a national problem.